[Updated 1 March 2020: On 4 February 2020 the insurer filed its brief. Go here for a copy. Here’s what they said about this post:

With the law and rules of grammar against them, the insureds scour the Internet in search of support for their efforts to transform a stylistic choice into an ambiguity. The insureds settle on a blogger—one who has never been cited as authoritative by either this Court or a Florida state or federal court. (Insureds’ Br. at 48-50) The insureds’ reliance on this blogger is self-defeating, given his belief that a serial comma “has nothing to do with what’s going on in this provision [the ‘Amusement Devices’ exclusion].” Kenneth A. Adams, Some Serious Comma Confusion Out of Florida, Adams on Contract Drafting (Nov. 5, 2019, updated Jan. 14, 2020), https://www.adamsdrafting.com/some-serious-comma-confusion-out-of-florida/.]

[Updated 14 January 2020: On 16 December 2019, the organizers of the event filed, as appellants, an initial brief with the United States Court of Appeals for the Eleventh Circuit. They cited this blog post extensively. I’m not surprised. Go here for a copy of their brief.]

People don’t understand commas. And that includes judges. Heck, we saw a comprehensive example of that in August, in this blog post.

Now we have more comma confusion, in the form of the opinion of Judge Carlos E. Mendoza of the U.S. District Court for the Middle District of Florida in Princeton Excess & Surplus Lines Insurance Co. v. Hub City Enterprises, Inc., No. 6:18-cv-1608-Orl-41GJK (M.D. Fla. Oct. 3, 2019) (PDF here).

That case involved someone who attended “Rum Fest 2017” and hurt his arms fending off an “extra-large inflatable beach ball.” (I can’t wait for Rum Fest 2020!) The organizers sought to have their insurer handle the matter, but instead the insurer sued, asking the court to hold that because the beach ball fell within an exclusion covering “amusement devices,” the insurer wasn’t required to defend the tort claim brought by the injured gentleman.

Misdiagnosis

The first issue was whether the “amusement device” exclusion applied to this claim; the judge concluded that it did. (I won’t consider the next issue, namely whether the beach ball was an amusement device.) Here’s the part of the insurance policy that relates to the first issue:

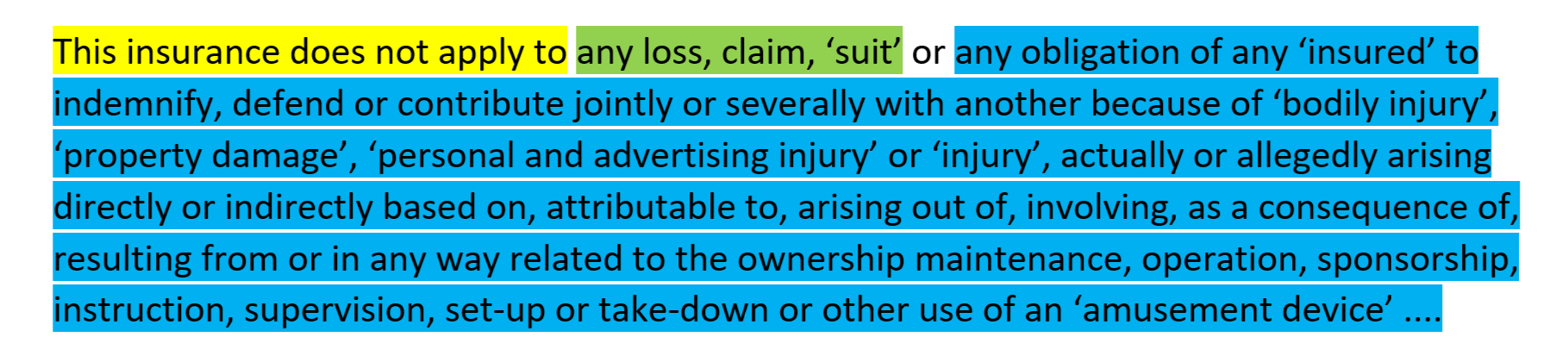

This insurance does not apply to any loss, claim, ‘suit’ or any obligation of any ‘insured’ to indemnify, defend or contribute jointly or severally with another because of ‘bodily injury’, ‘property damage’, ‘personal and advertising injury’ or ‘injury’, actually or allegedly arising directly or indirectly based on, attributable to, arising out of, involving, as a consequence of, resulting from or in any way related to the ownership maintenance, operation, sponsorship, instruction, supervision, set-up or take-down or other use of an ‘amusement device’ ….

No one had anything helpful to say about this language—not the lawyers for the organizers, not the lawyers for the insurer, and not the court. We’re interested only in what the court had to say:

The amusement device exclusion in its entirety presents a strong argument for use of the serial comma. Nevertheless, it is entirely common and accepted in American English for the final item in a list to not be preceded by a comma. The exclusion contains multiple such lists. And, when the exclusion is read as a whole, it is clear that the final item on each list is meant as a final item and not as a modifier for the other items on each list. For the clause at issue here, the clearest reading is: “[t]his insurance does not apply to any loss, claim, ‘suit[,]’ or any obligation ….” In other words, the insurance does not apply to any: loss, or claim, or suit, or obligation. And, the phrase “to indemnify, defend or contribute” only modifies “obligation.” Indeed, that very clause supports the Court’s reading. Clearly, it would be appropriate for a comma to be placed in between “defend” and “or contribute” because contribute does not modify defend but is another obligation of any insured.

Some problems:

- The serial comma—the comma before an and or or between the final two items in a list of three or more—has nothing to do with what’s going on in this provision. More specifically, MSCD ¶¶ 12.57–.76 describes three kinds of confusion that could be remedied by a serial comma: inadvertent combined elements, inadvertent apposition, and inadvertent object of preposition. None of the three appears in this provision.

- The final item in a list never modifies the other items in the list. For example, there’s no basis for saying that in the phrase a red, blue, green, or yellow ball the word yellow somehow modifies the words red, blue, and green.

- The judge suggests that the “clearest reading” involves adding a serial comma after suit, but he doesn’t say what the two or more other possible meanings are. (If there were just one other possible meaning, presumably he would have said “clearer.”)

- A comma added after suit wouldn’t be a serial comma—the any before obligation turns the noun phrase beginning obligation into a separate object of the sentence, with the nouns loss, claim, and suit serving as an initial group of objects. A comma after suit would have to serve some other purpose.

- To understand this language, you shouldn’t limit yourself to the initial part.

- Yes, the phrase to indemnify, defend or contribute modifies just obligation (to indemnify, defend, or contribute is the beginning of an infinitive phrase that acts as an adjective describing obligation). But that’s because of the any before obligation.

- Putting a comma after defend wouldn’t change the meaning. In particular, contribute cannot somehow modify defend.

Some Actual Confusion

Here instead is the only source of confusion I spotted in the language at issue.

As I say in point 4 above, the most natural reading, grammatically, is that the sentence contains an initial group of subjects consisting of the nouns loss, claim, and suit (in green in illustration below) followed by a further subject, the lengthy noun phrase built around obligation (in blue).

But that reading doesn’t make sense: if the insurance doesn’t apply to any loss, claim, or suit, then presumably the insurance doesn’t cover anything. And that initial exclusion subsumes the second, narrower exclusion.

But that reading doesn’t make sense: if the insurance doesn’t apply to any loss, claim, or suit, then presumably the insurance doesn’t cover anything. And that initial exclusion subsumes the second, narrower exclusion.

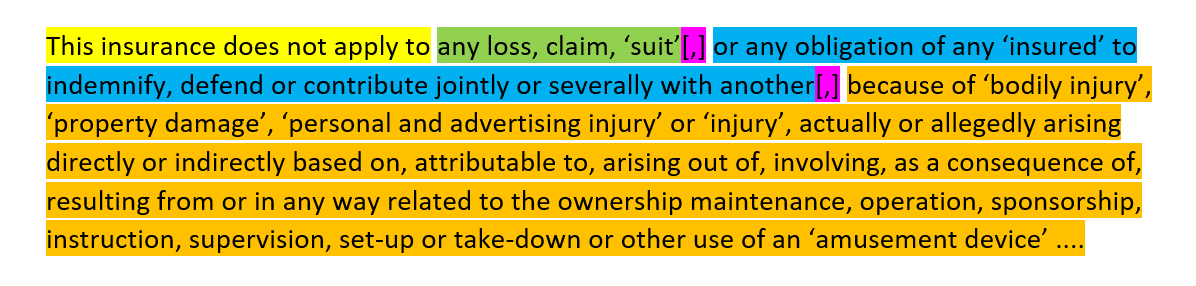

Here’s the most plausible alternative reading I could come up with:

In this version, the initial object group and the obligation object are modified by the lengthy prepositional phrase that follows. But for that to be clear, you’d have to add the offsetting commas (highlighted in pink).

But even if you do that, questions remain. For one thing, is the obligation element redundant, given the broad scope of “any loss, claim, ‘suit’”? And using because with obligation seems an odd choice.

If I were the judge, I’d say that the alternative version offered above requires too much work on the part of the court. That would leave the court with a choice: either you decide that there’s no scenario in which the circumstances of this dispute don’t fall within the “amusement device” exclusion—that the problem with the first group of objects is an irrelevant glitch—or you decide that the problem with the first part brings the entire provision into question.

Lessons

What can we learn from this mess? Well, the language at issue is poor. No surprise there—dysfunctional contract drafting is the norm. (Insurance policies are a kind of contract.)

What’s more worrisome is the opinion. To be an effective judge, you need better-than-average semantic acuity. Judges often fall short in that department, and over the years I’ve written about some spectacular screw-ups. (See for example this 2015 article and this 2015 post.) That why I’ve argued that it’s self-deceiving for courts to refuse to accept expert-witness testimony on ambiguity. (See this 2009 post.)

But what’s on display in Judge Mendoza’s opinion in Hub City isn’t your average confusion. Instead, he’s floundering.

This kind of word salad is always a recipe for disaster. It may be dangerous to read this sort of thing too closely, but, ignoring the unhelpful comments from the judge, and putting some emphasis on the comma between ” ‘injury’ “and “actually”, would a plausible alternative reading be:

“This insurance does not apply to

[A] any loss, claim, [or] ‘suit’ or

[B] any obligation of any ‘insured’ to indemnify, defend or contribute jointly or severally with another because of ‘bodily injury’, ‘property damage’, ‘personal and advertising injury’ or ‘injury’,

[in either case] actually or allegedly arising directly or indirectly based on, attributable to, arising out of, involving, as a consequence of, resulting from or in any way related to the ownership maintenance, operation, sponsorship, instruction, supervision, set-up or take-down or other use of an ‘amusement device’ ”

That is, it excludes all losses etc, and any obligations to indemnify etc due to bodily or other injury, if they arise in some way from an “amusement device” ? (In this case, does the claim arise from an amusement device? Yes it does. Case closed.)

Yeah, what he said!

Thank you for playing! To use Chris’s way of expressing it, you’re moving the blue in my second illustration to just before actually. The whole thing is so effed up that I don’t know whether it’s feasible to try to interpret it rationally, but my reservation with your suggestion is that it’s odd to refer to a claim (as opposed to an injury) as allegedly arising from something.

You are welcome. Glad to see that Chris and I are on the same page – that is, if the ball is an “amusement device”, and this case arises from such a device, then the plain words of the policy indicate such cases should be excluded. Perhaps the judge shared that opinion, but rather than just saying something simple like that instead wanted to impress everyone with textual analysis, with rather unfortunate results).

I don’t see a difficult in speaking about a claim (either a claim by a third party against the insured for which the insured is seeking protection under the insurance policy, or a claim by the insured for their own loss under the insurance policy) or a suit (ditto) “actually or allegedly arising directly or indirectly … from … use of an ‘amusement device’ “.

At the end of the day the judge needs to try to work out what the parties meant, and I think a judge is entitled to take a rather broad-brush common sense approach to such convoluted drafting.

If I had to write something like this, I’d be tempted to bury all of the defensive drafting in definitions and interpretation clauses, and just say something simple like “This insurance does not apply to any Loss arising from an Amusement Device.”

Ken:

What if you extended the blue down to just before the word “actually”? Wouldn’t that be a workable reading?

Chris

You troublemaker! :-) See my answer to Andrew above.

Doesn’t the inclusion of the offsetting commas in your final alternative reading (which I agree is the most plausible) show that the comma exclusion to the rule of the last antecedent does make sense?

Hi Neal. The comma-means-it-modifies-everything rule and the effect of offsetting commas are two different mechanisms. In some cases you can apply both to the same effect, but the former is applied more broadly, in circumstances where offsetting commas are absent. The fact that proponents of the comma-means-it-modifies-everything rule can sometimes be right for the wrong reasons isn’t to their credit.

Can you give me an example of language in which the modifier is immediately preceded by a comma, but that doesn’t involve offsetting commas?

Unfortunately I’m not in a position to dive back into this at the moment. The alpha and omega of my understanding of the comma thing is in my 2015 law-review article, at https://www.adamsdrafting.com/wp/wp-content/uploads/2015/08/Bamboozled-by-a-Comma.pdf. If it doesn’t answer your question, let me know.